Why Filming in Mexico Just Got Cheaper for US Producers

Mexico has long been a preferred destination for international film and audiovisual productions — exceptional locations, competitive crew rates, and a deep production infrastructure. But for US producers, one question consistently arises before a single camera rolls: what does filming in Mexico actually cost once taxes are factored in?

In 2026, the answer changed. A combination of long-standing VAT exemption rules and a landmark 30% federal tax credit introduced by presidential decree means international producers can now film in Mexico with both financial efficiency and full legal certainty. This guide walks you through how Mexico film tax incentives actually work, who qualifies, and how to structure your production so the benefit isn’t lost to a paperwork error.

How the 0% VAT Rule Works for International Productions

Mexico’s standard VAT rate (IVA) is 16%, administered by the Servicio de Administración Tributaria (SAT). For international film and video productions, however, a critical exemption applies: productions shot in Mexico whose primary exploitation will occur outside the country are classified as an exported service, and qualify for a 0% VAT rate.

In practice, this can recover 16% of a multi-million-dollar local spend — but only if the production is structured correctly from day one.

Requirements to Invoice Production Expenses at 0% VAT

- All qualifying expenses must be billed through a single Mexican entity (typically a production services company or an SPV).

- That entity must obtain prior authorization from SAT before invoicing begins.

- All invoices must be issued as CFDI (Comprobante Fiscal Digital por Internet) compliant with SAT standards.

- The production must be able to demonstrate that its primary distribution and exploitation is outside Mexican territory — distribution agreements, financing documents, and chain-of-title all matter here.

The 0% rate is not retroactive. Productions that invoice at 16% and try to reclaim it later usually lose the benefit.

The 2026 Presidential Decree: A 30% Tax Credit for Audiovisual Productions

On February 16, 2026, the federal government published a decree in the Official Gazette of the Federation granting a transferable income tax credit of up to 30% of qualifying Mexico-incurred film and audiovisual costs. Implementation guidelines followed on March 30, 2026, and the program is open through September 30, 2030 (see KPMG’s summary and Baker McKenzie’s analysis).

The credit is capped at MXN 40 million per beneficiary and MXN 400 million annually across the program — meaning early applicants with prepared documentation have a real first-mover advantage.

Who Qualifies (and Who Doesn’t)

Eligible projects include narrative and animated feature films, episodic series, documentary features and series, and standalone animation, VFX, or post-production processes. To qualify, a project must:

- Spend the required minimum within Mexican national territory.

- Use at least 70% national suppliers for goods and services.

- Submit to the Technical Committee, obtain a processing certificate, and ultimately a certificate of compliance.

Foreign individuals and legal entities can qualify if they hold a permanent establishment in Mexico or — more commonly for US producers — produce through a Mexican production entity that contracts and pays the local spend.

Minimum Investment Thresholds

- Narrative or animated features / series episodes: MXN 40 million minimum spend (~USD 2.3M).

- Documentary features or series: MXN 20 million.

- Standalone animation, VFX, or post-production processes: MXN 5 million per process.

How to Apply Through a Mexican Production Entity

The credit is not a reimbursement and it is not automatic. A workable application sequence looks like this:

- Engage a Mexican production services entity with SAT registration and a clean compliance record.

- Confirm category, projected spend, and the 70% national-supplier ratio before committing to budgets.

- Submit the project to the Technical Committee for the processing certificate.

- Track qualifying spend in CFDI format throughout production.

- Apply for the certificate of compliance at wrap, then claim or transfer the credit.

Productions that try to retrofit this process post-shoot routinely lose eligibility (Bloomberg Tax coverage).

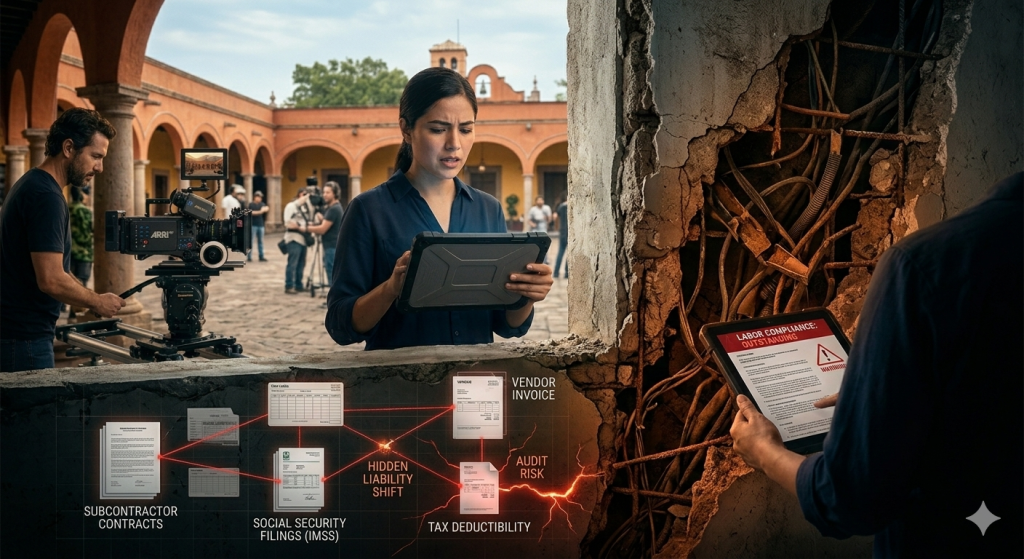

Why Legal Structure Is a Competitive Advantage in Mexico

For US producers who approach Mexico with a structured legal strategy, compliance becomes a competitive advantage. With properly vetted production-services partners, clean payroll structures, and continuous verification of social-security and tax filings, uncertainty is transformed into predictability.

Mexico rewards preparation. When the legal framework is designed before the cameras roll, productions gain access to mechanisms that materially reduce costs:

- Exported-service VAT treatment at 0%.

- Fiscally efficient co-production models under the 2026 decree.

- Audit readiness for future distribution, sale, and corporate governance.

If you need help thinking through how this fits a specific budget, we cover the same ground from the labor-law side in Payment Liability in Mexico: What US Film Producers Must Understand Before Hiring Crew and the permitting side in Filming in Mexico: Legal Requirements for Foreign Productions.

Prevention: What International Producers Actually Value

What international producers increasingly prioritize is not aggressive enforcement after a problem arises — it’s the ability to prevent the problem from existing at all.

A production that is compliant from day one benefits from a seamless workflow:

- It does not attract unnecessary SAT inspections.

- It avoids bottlenecks in permitting and logistics.

- It eliminates financial surprises months after wrap.

Creative decisions stay creative, schedules stay intact, and Mexico delivers on its promise as a reliable production partner rather than a jurisdiction to be managed defensively. We unpack this idea in more depth in Filming in Mexico: Why Legal Certainty is the New Production Asset for US Producers.

Conclusion: Treat Legal Structure as Production Design

The future of producing in Mexico belongs to teams that treat legal structure as a core element of production design, not as an afterthought. For US producers willing to adopt this mindset, Mexico is not simply an alternative market — it is a strategic extension of the production pipeline, with a combined 0% VAT exemption and 30% federal tax credit that few other jurisdictions can match.

Planning a shoot in Mexico in the next 12 months? Contact ANFEPA for a structuring review before you lock budgets.

FAQ: Mexico Film Tax Incentives at a Glance

What is the 30% film tax credit in Mexico?

A transferable federal income tax credit of up to 30% of qualifying Mexico-incurred film and audiovisual costs, introduced by presidential decree on February 16, 2026 and in force through September 30, 2030.

Can US producers claim Mexico’s 30% film tax credit?

Yes — provided the production runs through a Mexican production entity (or has a permanent establishment in Mexico), meets the minimum spend threshold, and uses at least 70% national suppliers.

Is filming in Mexico exempt from VAT?

Productions whose primary exploitation occurs outside Mexico can be invoiced at a 0% VAT rate as an exported service, but only when billed through a single SAT-authorized Mexican entity using compliant CFDI invoices.

What is the minimum spend to qualify for Mexico’s film tax credit?

MXN 40 million for narrative/animated features and series; MXN 20 million for documentary features and series; MXN 5 million per process for standalone animation, VFX, or post-production work.

When does Mexico’s 2026 film tax credit decree expire?

The program is in force until September 30, 2030, subject to annual caps of MXN 400 million.